Oil Explodes and Catches Bitcoin in the Blast Radius

Understand the scale of disruption and the market outlook

Tough times for markets. The Iran war has changed the market fundamentals and has disrupted one of the most consequential energy commodities. This is no small disruption with wild effects on markets.

In the past few days, I have seen a lot of panic and doom-and-gloom posts on social media (“worst disruption in the history”, etc., etc.). Markets pump and dump on every piece of negotiation news. And investors are likely to make decisions they will regret in the long term.

And this is a key issue for Bitcoiners too. The outlook for Bitcoin and oil is now tied together.

So I decided to dedicate this edition of the newsletter to researching the energy disruption and investigating how things may progress from here.

The Choke

Let’s acknowledge that the war’s ramifications are massive. In moments like this, the public discussion gets noisy fast. Political opinions get mixed with macro analysis, worst-case scenarios always get the most attention, and it becomes hard to tell what is actually happening versus what the market merely fears could happen.

The Iran war has triggered a violent repricing in oil and in a range of related commodities. Oil shocks do not stay contained to oil for long. They can spread to inflation expectations, growth forecasts, Fed expectations, equities, and eventually Bitcoin through the broader liquidity and risk environment.

The first thing to establish is that the market reaction has good reasons.

WTI crude has exploded higher over a short period, moving from a relatively calm range into the $90–$100 zone. Traders are pricing a real and sustained supply risk.

The war has largely blocked the traffic in the Strait of Hormuz, through which roughly a fifth of global oil flows, and the conflict is now in its fifth week. Oil prices rose about 50% over March, making it one of the steepest monthly rallies on record.

Commercial ship traffic through Hormuz collapsed to near-zero levels. Even if one argues later that not all lost traffic translates one-for-one into permanently lost supply, this is still evidence of a real operational shock.

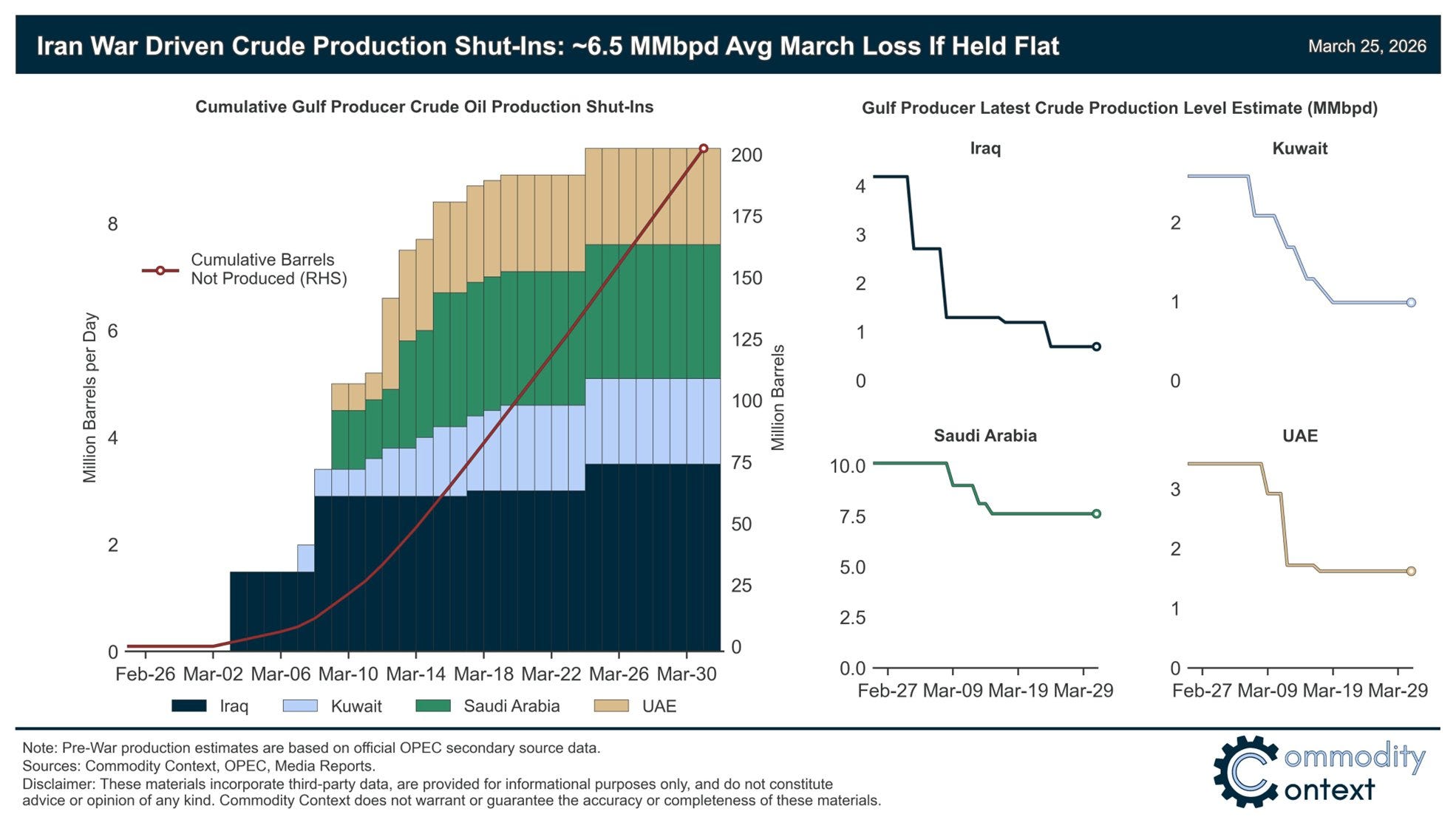

Production is actually getting stranded or cut as well.

Estimates point to an initial disruption of roughly 6.5 million barrels per day of Persian Gulf production shut-ins. Cumulative lost output is already measured at around 200 million barrels. A multi-week disruption becomes a compounding supply loss, getting worse by the day.

This shock could exceed the feared Russian supply loss of 2022 by a wide margin. Spare capacity is trapped behind Hormuz, inventories are lower, freight is less flexible, product markets are tighter, and the buffer between a manageable disruption and a disorderly price spike has become dangerously thin.

The Big Reroute Most Have Missed

That said, there is a major caveat that oil producing countries have not been idle. They are responding strategically.

Saudi Arabia has been investing in an alternative export route on the Red Sea, Yanbu, to circumvent the Strait. Its exports from Yanbu ramped toward 5 million barrels per day. That rerouting may have offset roughly 45% of lost Persian Gulf shipments. While that does not eliminate the shock, it does mean that Hormuz charts you see everywhere are missing the second-order effects and the alternative export routes. The oil system is under stress, but it is not helpless. It can adapt at the margin.

The shock is real, it is large enough to matter, but the final scale depends on how much rerouting, adaptation, and eventual reopening the system can achieve.

One War and 8 Global Shortages:

One reason the market is taking this so seriously is that it is not just an oil story. Liquefied natural gas, phosphate, helium, sulfur, urea, fertilizer, diesel, gasoline, coal, and even aluminum are under pressure too.

Markets are seeing a broad commodity squeeze. These are some of the price increases since the start of the Iran war:

Heating Oil: +77%

European Natural Gas: +71%

Brent Crude Oil: +58%

WTI Crude Oil: +51%

Urea: +48%

Diesel: +44%

Sulfur: +43%

Gasoline: +42%

Fertilizer: +29%

Coal: +21%

Palm Oil: +14%

Iron Ore: +7%

Rice: +7%

US Natural Gas: +6%

Inflation or Deflation?

The simple inflationary case is obvious enough: higher energy and commodity prices push up input costs and raise the risk of a headline CPI spike.

But there is a strong counterpoint. Energy is only a modest 7% share of CPI relative to housing which is 40%. Housing currently remains under immense pressure, and oil alone may not be enough to create a lasting inflation breakout.

On top of that, high oil is often inflationary in the short run but disinflationary later because it weakens consumption and demand. In other words, an oil shock can raise inflation prints while simultaneously undermining the growth that would be needed to sustain broad inflation.

The inflation expectations chart above suggests that markets are treating the current oil shock mainly as a near-term inflation problem, not yet as a full-blown long-term inflation regime shift.

As oil rises, shorter-term inflation expectations move higher because traders naturally expect energy costs to feed into headline CPI over the coming months.

But the more important measure here is the 5y5y forward inflation rate, which captures the market’s expected average inflation over a five-year period that begins five years from now. In other words, it is a gauge of longer-run inflation expectations rather than immediate price pressure.

Since that measure remains relatively contained while front-end expectations have risen, it shows the markets see the oil shock as inflationary only in the short run not the long run.

Growth, Recession, and Why This Time May Still Be Different

Historically, oil spikes have mattered because they hit both consumers and businesses at the same time. They act like a tax on the economy.

Every US recession from the 1970s through the Global Financial Crisis coincided with a doubling in oil prices, and while the 2022 Russia-Ukraine oil spike did not trigger a formal recession, it came close.

Markets are rational to worry when oil moves this violently. Large oil spikes and growth stress tend to appear together.

Now, another caveat for the United States comes from the gas market. The key difference between this shock and many older energy crises is the relatively muted impact on US natural gas. That is also not covered nearly enough as far as I have seen.

Natural gas feeds directly into industrial activity, electricity costs, and therefore into the broader inflation-growth mix. If US natural gas is not exploding, then the pass-through into the real economy may be less severe than the oil panic suggests.

This helps explain why the White House can tolerate more energy pain from Hormuz disruption than many observers assume. Oil hurts, but subdued US gas makes the shock less overwhelming than prior episodes.

The Fed Question

One of the fastest market reactions to any oil spike is a repricing of Fed expectations. People are now worried about a resurgence of inflation causing the Fed to hike rates again.

Goldman Sachs pushes back maintaining that history is not that mechanical. In 1990, markets expected tightening after an oil shock, but the Fed ultimately cut as growth weakened.

Oil shocks can produce an inflation scare first and a growth scare second. If the growth damage becomes dominant, the Fed may not end up where the market initially expects.

That point matters for Bitcoin as much as it matters for bonds or equities. If the market is misreading the sequence, it can price the wrong thing first. It can sell risk on inflation fear, then later reverse once growth weakens enough to reopen the conversation around cuts, liquidity support, or at least a less hawkish path. The path really matters here.

What Happens Next – Goldman Scenarios

Goldman Sachs research highlights three possible broad scenarios.

The first is a shorter disruption. In that case, oil spikes toward roughly $120 and then falls back sharply, perhaps toward $80.

The second is a more prolonged disruption without lasting infrastructure damage. In that world, oil spikes higher, maybe toward $140, and then settles into a structurally firmer range around the mid-$90s or higher.

The third is the worst case: prolonged disruption with production scarring, which drives oil toward $160 and keeps it above $100 on a more durable basis.

The key point is that the likely path is a spike first that will cause much consternation in the markets, followed by a sharp drop, likely not back to the old level and to a plateau of modestly higher prices.

The US has not Played All the Cards Yet

Another reason to be cautious about the most apocalyptic scenarios is that the United States has not yet exhausted its options. Commentators often jump too quickly to definite conclusions, as if the current state of the Strait must persist unchecked. That is a mistake.

The US still has economic, military, logistical, and diplomatic tools that could alter the path of this crisis, even if those tools have not yet been fully deployed or are not visible in real time to outside observers. If one thinks the most powerful military on earth has run out of ammo in dealing with the IRGC, they are in for a rude awakening.

In situations like this, the market often prices the shock in its current form while underestimating the probability of an active response that changes the setup.

The US has so far been using the safest methods of warfare: raining bombs. If push comes to shove, the US can explore more expensive options, such as land operations in the Persian Gulf region and taking over several islands used to make the Strait unsafe. They have been preparing for this scenario by deploying Marines and substantial military assets.

Another thing that can happen is that the Arab states, NATO members, and European countries could also conclude that allowing the IRGC to threaten global shipping is untenable and move to support maritime security.

If such operations are successfully carried out, the outlook will almost instantaneously change, and the oil price will plummet. Oil is not only a function of lost barrels today, but also of how credible a future restoration of flows appears to be. The more investors believe that blocked flows can eventually be reopened, the more likely it is that today’s shock proves violent but temporary rather than the start of a lasting energy regime shift.

This scenario is not discussed enough.

Iran is not Vietnam, Iraq, or Afghanistan. The objectives are different, the region is different, the technology is different, and the range of available US options is different.

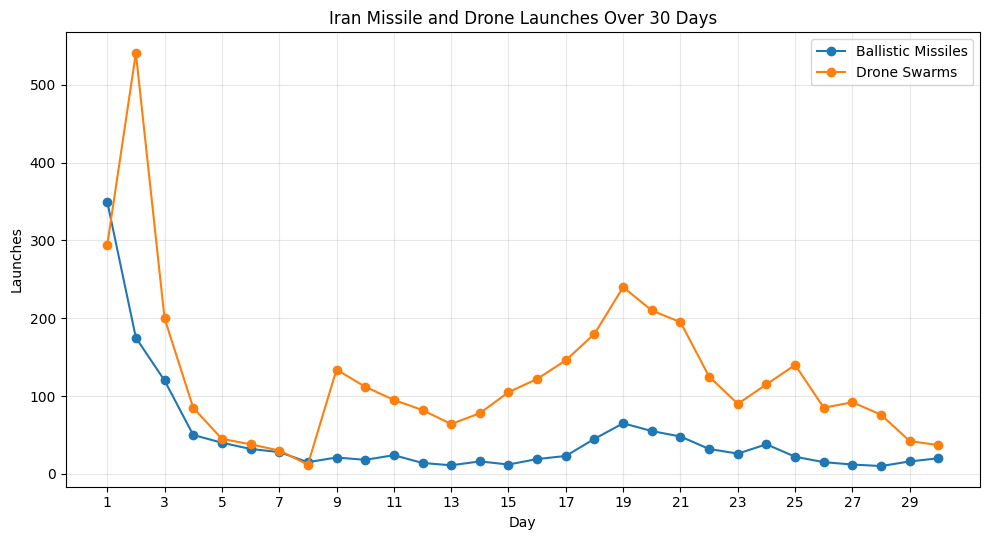

Note below how Iran’s missile and drone capacity has been degraded over time. That mid-chart surge made many believe that Iran is back on track, only to find that the US and Israel's campaign is materially destroying Iran’s ability to project power. Iran’s military production facilities have also been hit hard, making it unlikely that they can replace the used ammunition and more likely for this trend to continue. As their ammunition depletes and fire capacity degrades every day, there will come a day when their grip on the Strait will loosen materially. I am sure this will come as a surprise to many analysts.

What It Means for Markets and Bitcoin

For risk assets and Bitcoin, the near-term can be ugly.

Rising oil, broader commodity stress, inflation fears, and recession risk are a bad combination. Equities do not like that setup. Credit does not like it either.

Usually markets panic about inflation first, then panic about growth, and only later settle on which one matters more.

Bitcoin is being hit inside that same macro sequence. Its long-term thesis has not changed, but getting repriced because it still trades within the broader global liquidity and risk regime. When oil shocks tighten financial conditions and investors de-risk, Bitcoin gets caught in the blast radius.

If this turns into a brief panic followed by reopening and lower oil, then Bitcoin likely recovers with the rest of risk assets. If it turns into a prolonged military gridlock, the environment stays harder. Eventually it can morph into a growth shock that ultimately pulls central banks back toward easier policy, then the later stages of the episode may end up constructive for Bitcoin even if the first phase is painful.

Our expectation is that the same will happen this time. Markets are slowly pricing in inflation, but before much of it materializes, a slowdown in growth will become apparent and reverse expectations for rate hikes. On the war front, we still believe the US and Israel’s military supremacy will surprise the markets as they use a variety of novel strategies to reopen the Strait. So the markets are likely to overestimate the energy shock and underestimate a relatively quick resolution.

We will be watching.

Thanks for making it here. Let me know what you think in the comments.

Best,

Sina.