Convexity Builds Beneath a Compressed Surface

Collectively, the options market is not forecasting direction. It is mapping where stability holds, and where it breaks.

Summary

The Bitcoin options market continues to reflect a regime of engineered stability rather than directional conviction. Near-dated positioning remains defensive, with downside protection concentrated below spot, while longer-dated expiries express persistent upside convexity through sustained call accumulation. This time-segmented structure suggests that participants are not positioning for immediate resolution, but rather insuring against deviation while retaining exposure to longer-horizon asymmetry.

Volatility remains compressed across both implied and realized measures. Short-term implied volatility exhibits episodic spikes that fade quickly, while longer-dated implied volatility remains stable and shallow. The absence of a meaningful term premium indicates that the market is not pricing a discrete catalyst, but instead maintaining optionality without urgency. Importantly, volatility is not being aggressively sold across the curve—compression reflects deferred risk, not complacency.

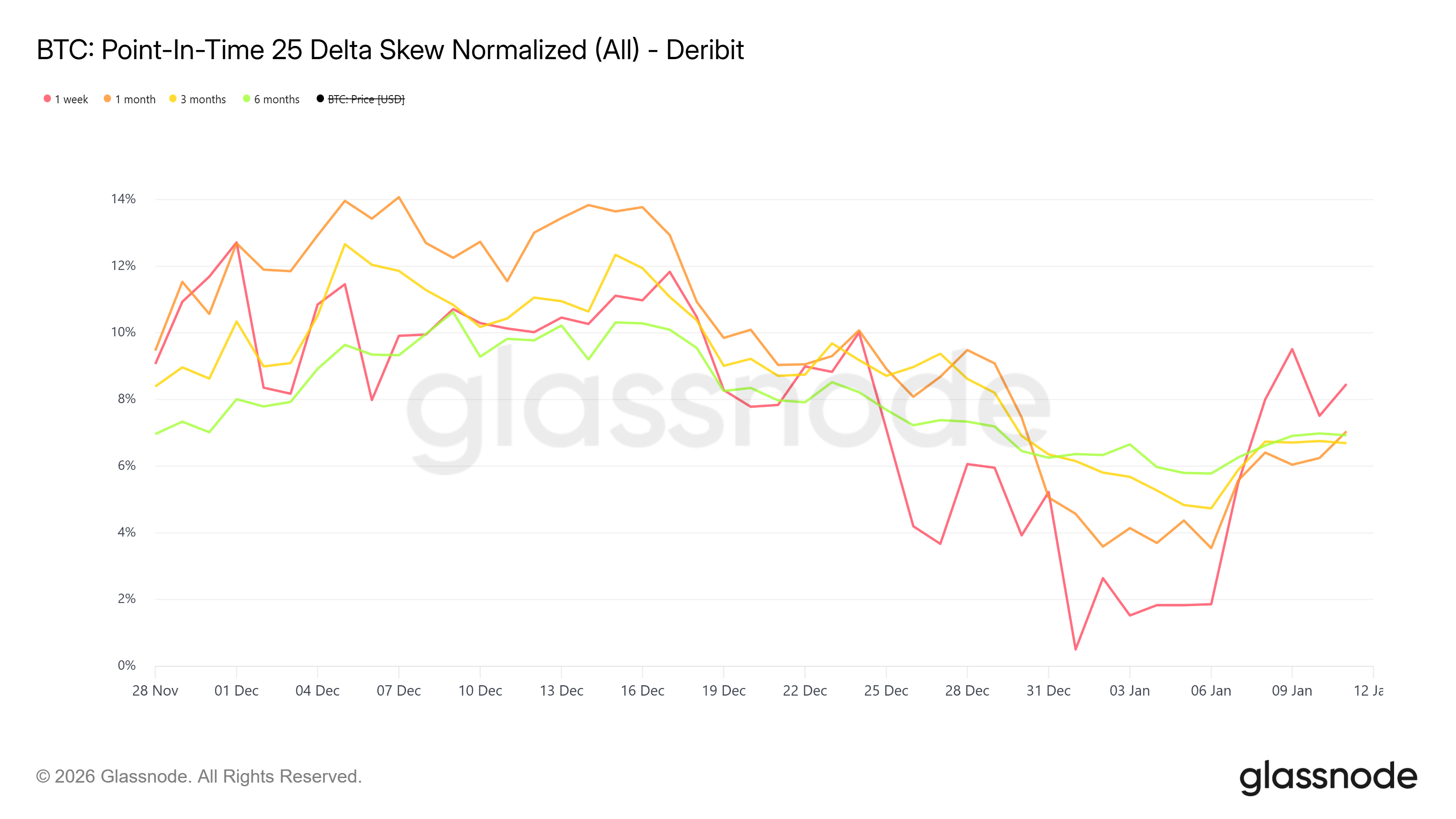

Skew dynamics reinforce this interpretation. Normalized 25-delta skew remains persistently negative across maturities, confirming sustained demand for downside convexity even as volatility compresses. The implied volatility smile remains stable and well-anchored, with minima clustered tightly around the prevailing spot regime and no evidence of distributional repricing. Uncertainty is being adjusted in level, not in shape.

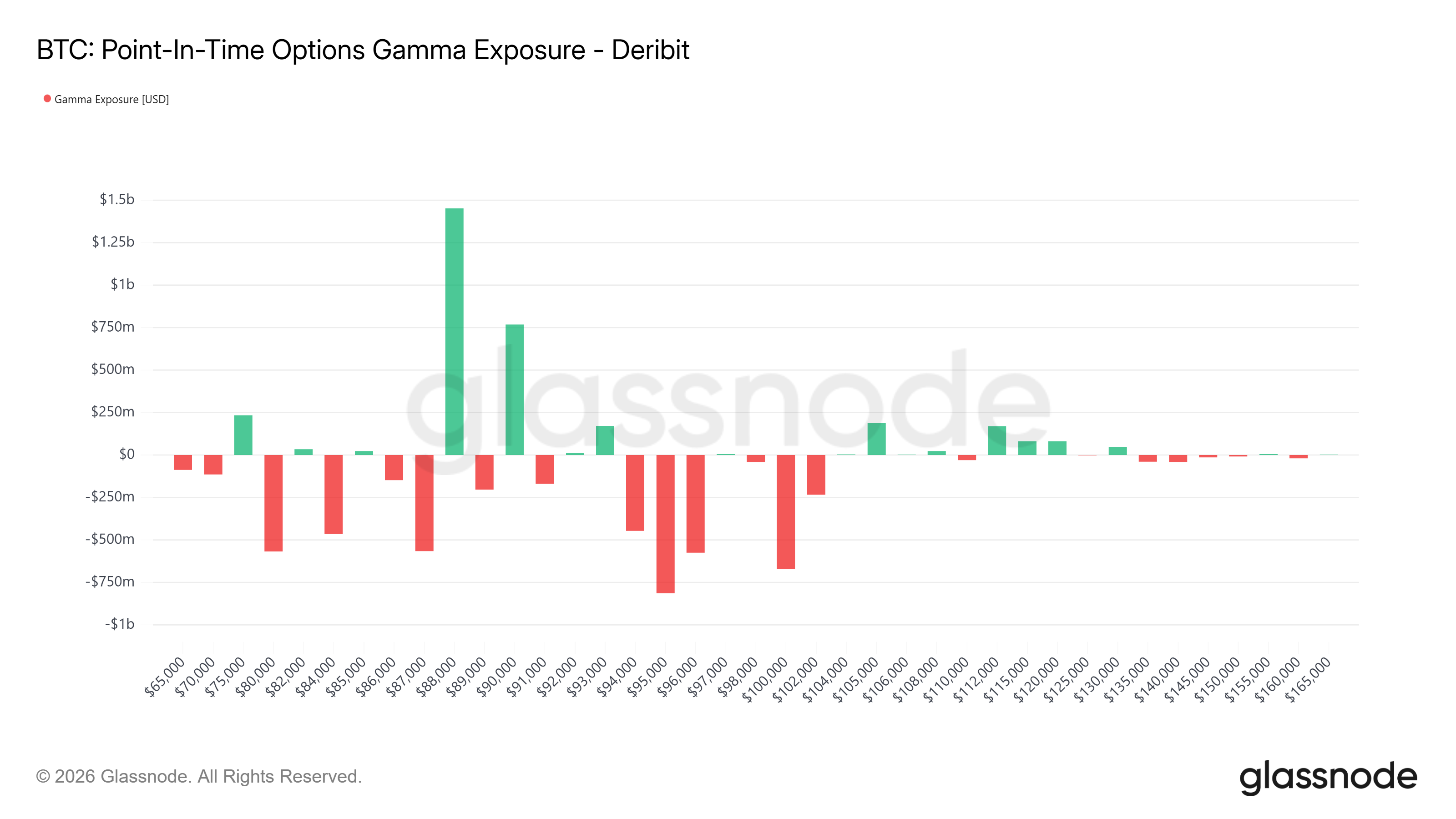

Dealer gamma exposure completes the picture. Point-in-time gamma reveals localized zones of stabilization around spot price, where price movement is dampened through hedging flows. Outside these regions, gamma thins rapidly, creating fragile boundaries where price can transition quickly from suppressed to amplified movement.

Collectively, the options market is not forecasting direction. It is mapping where stability holds, and where it breaks.

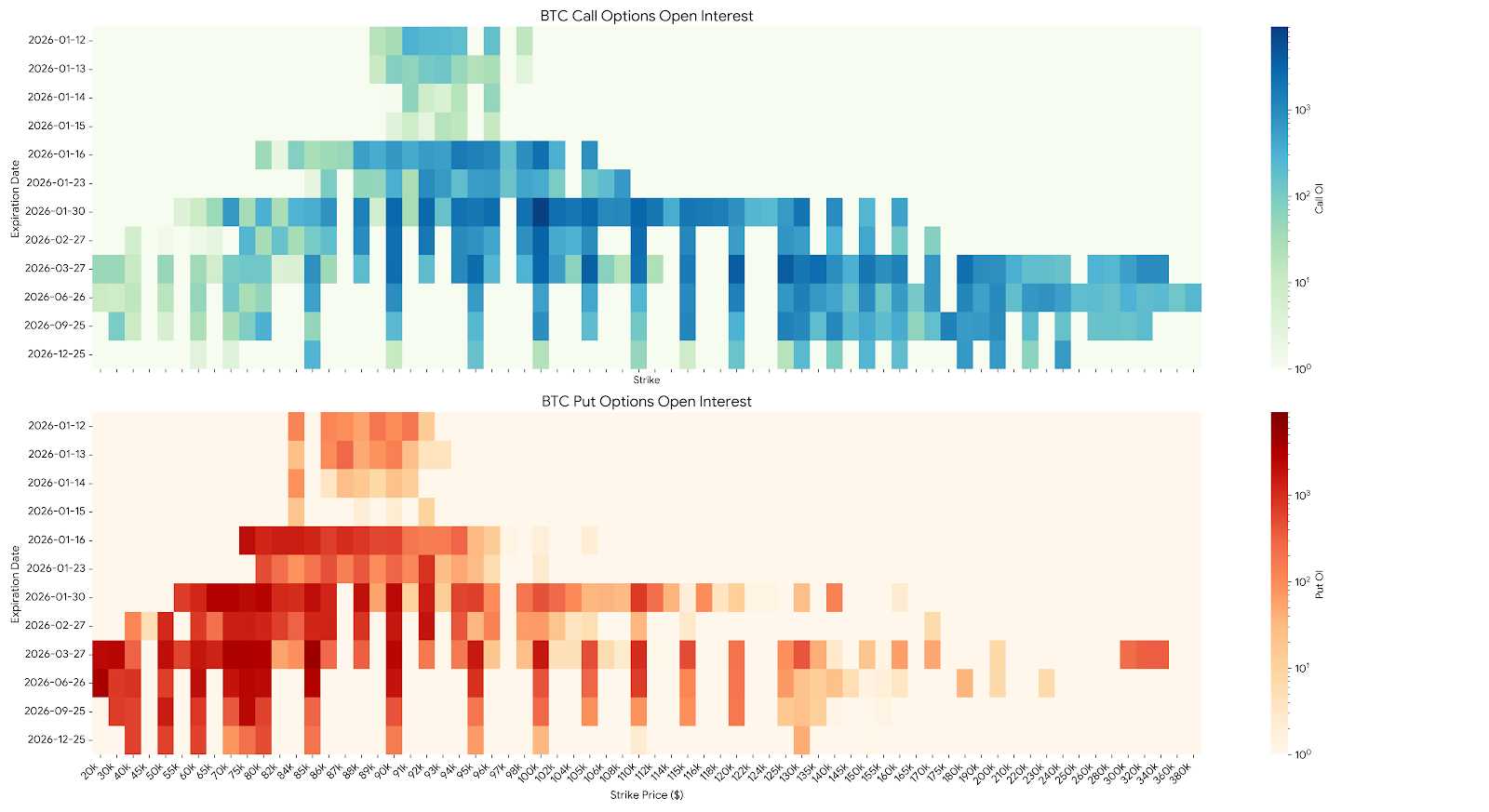

Open Interest: Downside Insurance Dominates Near-Term Positioning

The January 2026 options open interest profile highlights a market that remains primarily focused on downside risk management, with comparatively muted expression of short-term upside conviction.

Put open interest is concentrated across a broad range of strikes below the prevailing spot price, with the densest clusters forming between approximately $75k and $90k. This concentration is visible across multiple January expiries, indicating that downside protection is not tied to a single event or date, but rather reflects persistent hedging demand.

Importantly, the distribution of put open interest is diffuse rather than localized. Rather than a single dominant strike, exposure is spread across adjacent levels, suggesting that market participants are seeking range-based protection rather than positioning for a precise downside target. This structure typically acts to dampen incremental declines, as hedging flows absorb price movement within the insured zone.

By contrast, call open interest above spot is present but more evenly distributed across higher strikes. While longer-dated January expiries show meaningful call exposure extending well above current price levels, there is no single upside strike that dominates the profile. This indicates that upside exposure is being maintained in a conditional and non-aggressive manner, consistent with optional participation rather than directional conviction.

Around the immediate spot region, open interest on both the call and put side thins noticeably. The absence of a pronounced at-the-money concentration suggests that the market is not strongly anchored to a specific short-term outcome. Instead, positioning reflects a preference to define risk boundaries, rather than predict near-term price direction.

Taken together, the January open interest structure points to a market that is well-insured against downside moves, while remaining flexible on upside outcomes. This configuration is characteristic of periods where price discovery slows, volatility compresses, and participants prioritize capital preservation over tactical expression.

In such environments, price action often remains contained until one of the structurally significant regions of open interest is approached, at which point hedging dynamics can begin to exert a stronger influence on market behavior.

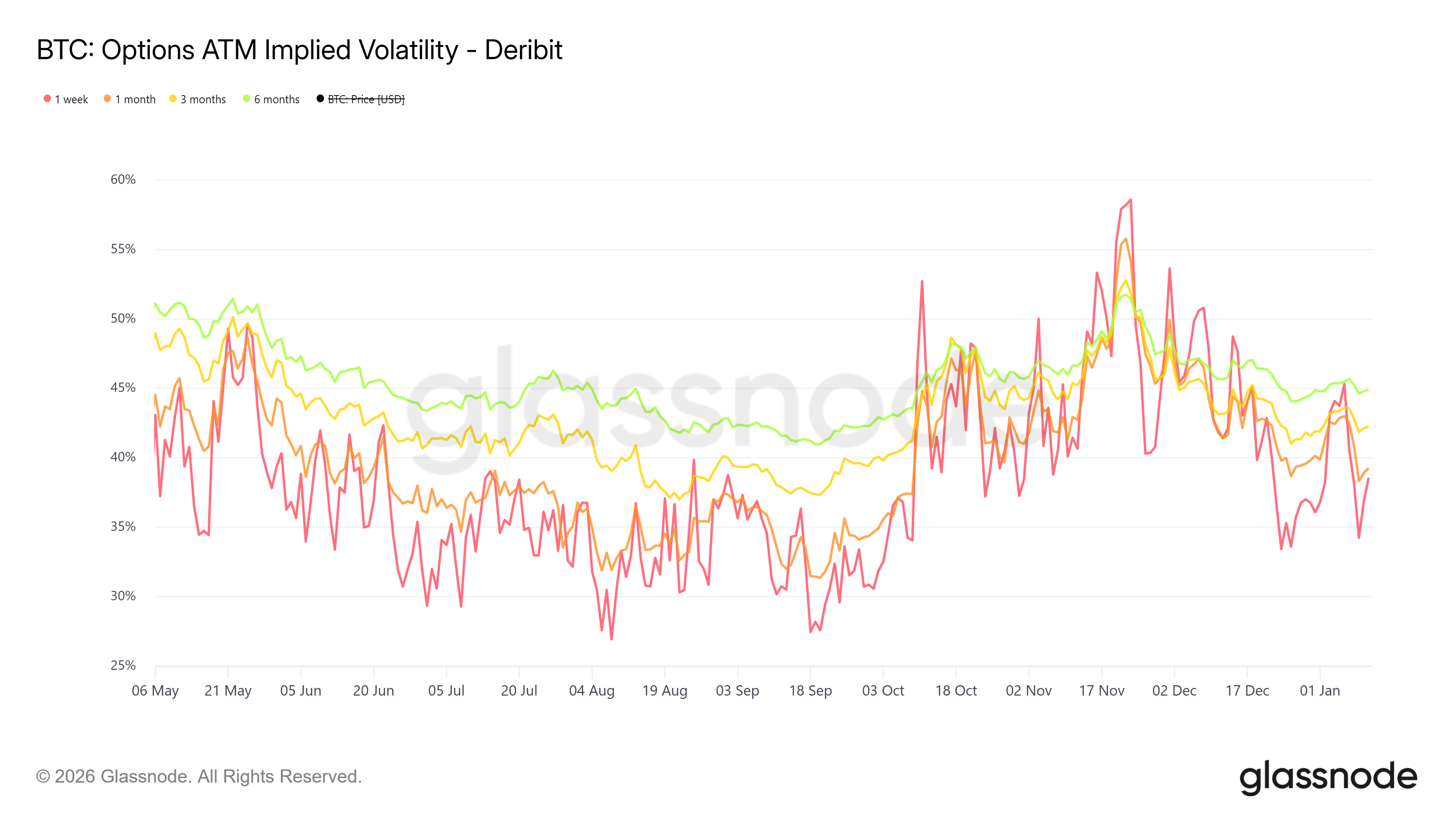

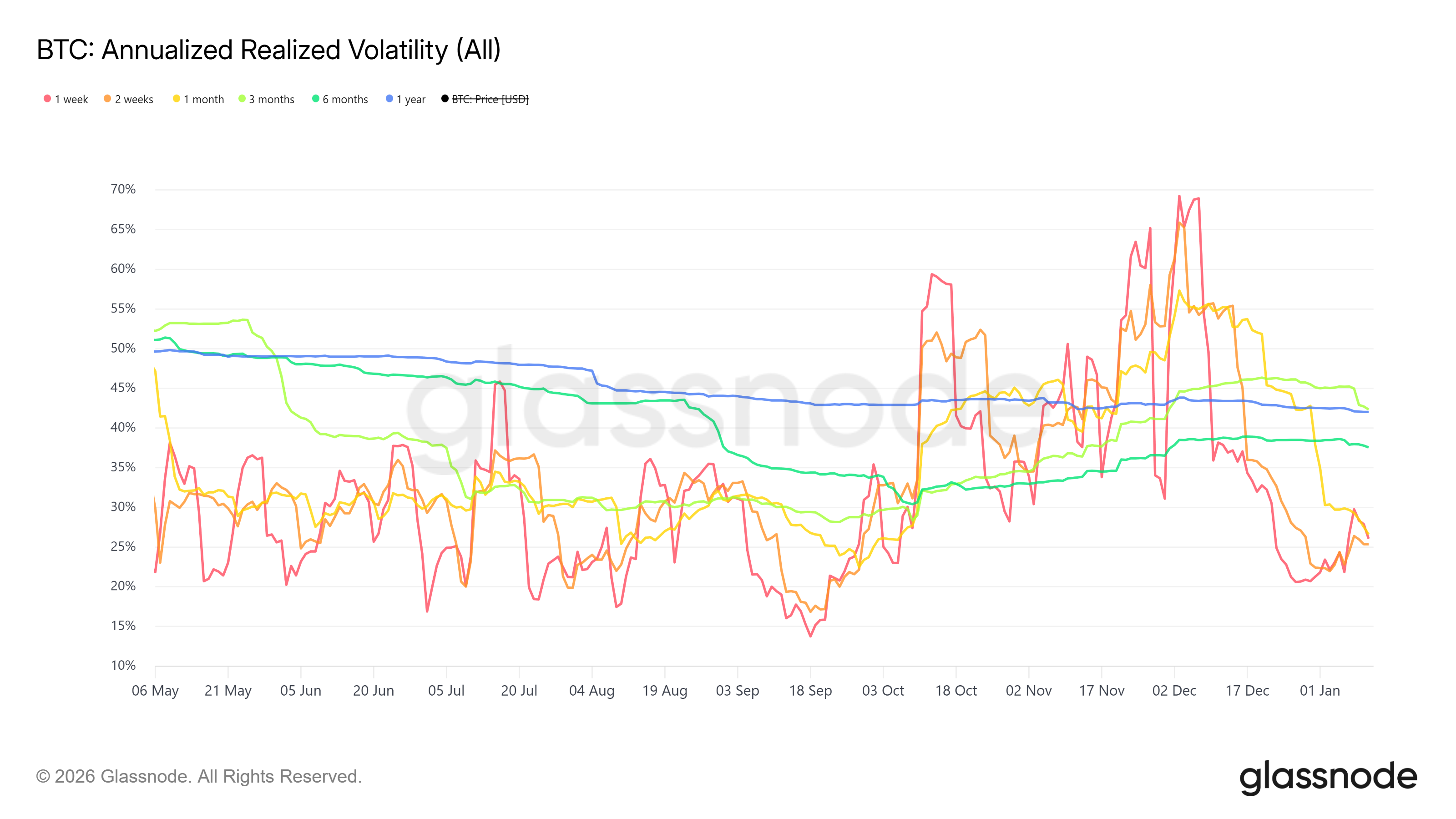

Volatility: Compression Persists as Risk Is Deferred

Across both implied and realized measures, the volatility regime remains characterized by compression rather than expansion, with short-term fluctuations occurring inside a broader, subdued envelope.

ATM implied volatility across tenors has trended lower since mid-year, with the 1-week and 1-month series displaying episodic spikes that fade quickly. These bursts coincide with short-lived price disturbances but fail to translate into a sustained repricing of forward risk. Longer-dated implied measures (3–6 months) remain comparatively stable, forming a shallow downward slope through the summer before modestly firming into late Q4.

Realized volatility tells a complementary story. Short-horizon realized measures exhibit pronounced noise, but collapse rapidly following each spike, reverting toward the low- to mid-20% range. Longer windows (3 months to 1 year) continue to grind lower, reinforcing the absence of persistent directional stress. The dispersion between short- and long-horizon realized volatility highlights a market experiencing transient shocks without regime change.

The relationship between implied and realized volatility remains asymmetric. While implied volatility consistently trades above realized, the premium is contained rather than stretched, indicating that the market is pricing uncertainty without signaling acute fear. In effect, volatility is being warehoused, not aggressively bid.

This configuration suggests that participants remain willing sellers of short-term movement, yet reluctant to relinquish optionality altogether. Volatility compression is therefore not a sign of complacency, but rather of deferred risk, where uncertainty is acknowledged but postponed.

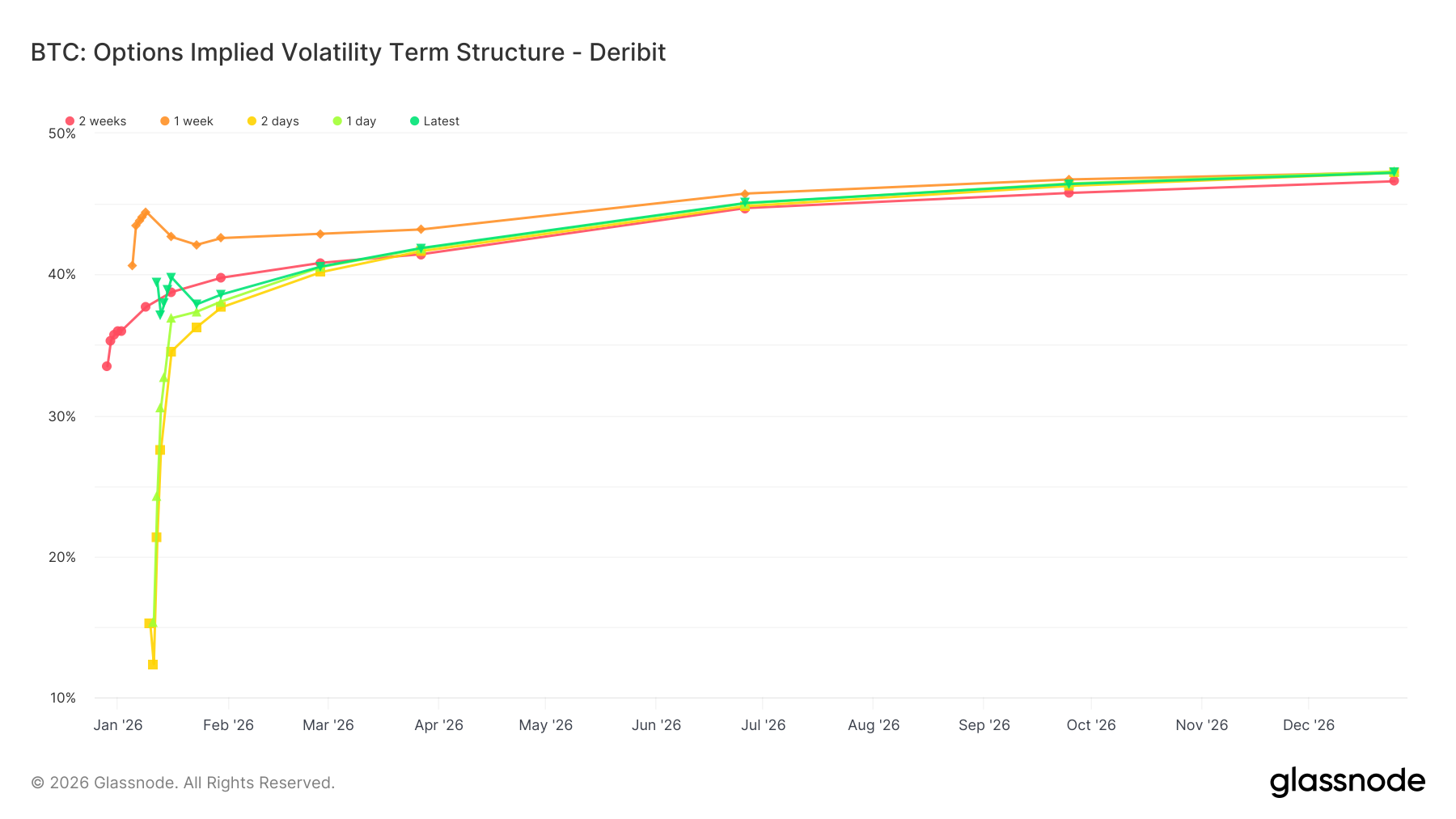

Term Structure and Skew: Protection Is Priced, Panic Is Not

The implied volatility term structure remains remarkably flat, with only a modest upward slope from front-month expiries into late-2026 maturities. Near-dated implied volatility sits in the mid-30s to high-30s range, while longer-dated tenors stabilize in the mid-40s. This configuration reflects a market that is not pricing an imminent volatility event, but is unwilling to significantly discount longer-horizon uncertainty.

Importantly, the front end of the curve has failed to invert or steepen, even during recent spot fluctuations. Short-dated implied volatility briefly reprices higher during local disturbances, but these moves are quickly absorbed without propagating up the curve. This behavior is characteristic of event-agnostic volatility demand, where protection is maintained structurally rather than tactically.

In parallel, normalized 25-delta skew remains consistently positive across maturities, confirming that downside options continue to command a volatility premium over equivalent upside structures. While short-term skew exhibits higher variability, particularly around late-December and early-January price moves, these dislocations are transient. Medium- and long-dated skew remains smooth and elevated, indicating that downside asymmetry is being priced deliberately, not reactively.

Notably, there is no sustained skew inversion at any tenor. Even during periods of implied volatility compression, the market does not transition into upside-dominant pricing. This absence of call-side exuberance reinforces the view that upside participation is being expressed selectively, while downside insurance remains a persistent fixture of the surface.

The coexistence of a flat term structure and positive skew conveys a clear message:

Risk is acknowledged, but not time-compressed. The market is willing to warehouse uncertainty over longer horizons while continuing to pay for near-term protection. This is not the posture of a market bracing for immediate instability, nor one positioned for runaway upside. It is the posture of a market operating under structural caution, where convexity is accumulated patiently rather than chased.

In the background, the implied volatility smile remains stable and well-anchored, reinforcing this interpretation. Across expiries, smile minima continue to cluster tightly around the prevailing spot regime, with no meaningful migration higher or lower. The left tail remains consistently steeper than the right, confirming that downside convexity is still priced more aggressively than upside, even as overall volatility compresses. Importantly, the smile shape has shifted largely in parallel rather than deforming, indicating that the market is adjusting the level of uncertainty without reassigning its distribution. This stability suggests that while risk is being actively managed, participants are not repositioning for a change in regime, but rather maintaining a structurally asymmetric view of outcomes.

Gamma Exposure: Stability With Fragile Boundaries

Point-in-time gamma exposure reveals a market structured around localized stability rather than broad directional conviction. Dealer positioning is unevenly distributed across strikes, creating alternating zones where price movement is either dampened or amplified.

Near the prevailing spot region, gamma exposure is predominantly positive, with several large positive gamma concentrations clustered just above and below the current price. In these zones, dealer hedging flows act counter-cyclically: dealers buy into weakness and sell into strength, mechanically suppressing volatility and encouraging mean-reverting price behavior.

However, this stabilizing influence is not continuous. Outside the core gamma cluster, exposure quickly flips negative, particularly at strikes further below spot. In these regions, dealer hedging becomes pro-cyclical, reinforcing price moves rather than resisting them. This creates fragile boundaries, where modest price excursions can transition rapidly into more directional movement once dominant gamma levels are breached.

The asymmetry in gamma distribution is notable. Downside strikes exhibit deeper and more concentrated negative gamma pockets than their upside counterparts. This aligns with the broader options structure: downside risk is insured, but once key protection levels are tested, hedging flows can accelerate price movement rather than cushion it.

Taken together, the gamma profile explains the current market texture. Price remains stable while it oscillates within the dominant positive gamma corridor, but becomes increasingly sensitive as it approaches structurally significant strikes. Stability, in this context, is engineered, not organic — and it persists only as long as price remains inside the boundaries defined by dealer positioning.

Final Thoughts

This is a market operating under structural constraints. Stability is not the result of confidence, but of positioning mechanics: downside is insured, volatility is warehoused, and convexity is accumulated patiently rather than chased.

Such regimes are inherently self-reinforcing—until they are not. The longer price remains confined within dominant gamma and strike concentrations, the more volatility is suppressed. Yet the same structure ensures that once price escapes these boundaries, adjustment is unlikely to be gradual. Hedging flows that dampen movement near spot price can rapidly flip into accelerants once key levels are breached.

The options market is therefore not signalling imminent stress, nor is it endorsing directional calm. It is signalling latent sensitivity. Volatility is not extinguished; it is stored. Resolution, when it arrives, will be dictated less by sentiment than by structure.

In this environment, the question is not whether instability emerges, but where it is released, and how quickly positioning must adapt once it does.

| A guest post by

|